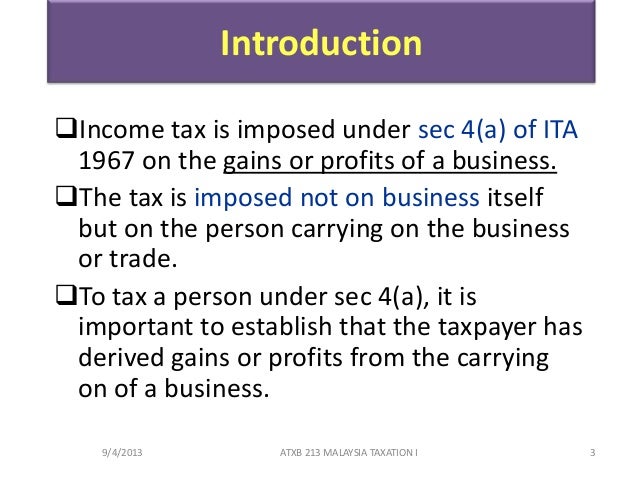

Section 4a Income Tax Act Malaysia

Taxation Principles Dividend Interest Rental Royalty And Other So

Chapter 8

Chapter 1

Ppt Tutorial 1 Introduction To Income Tax Law Powerpoint Presentation Id 3473088

Chapter 5 Non Business Income Students

Tax Planning On Rental Income Afc Chartered Accountants Audit Tax Advisory And Accounting

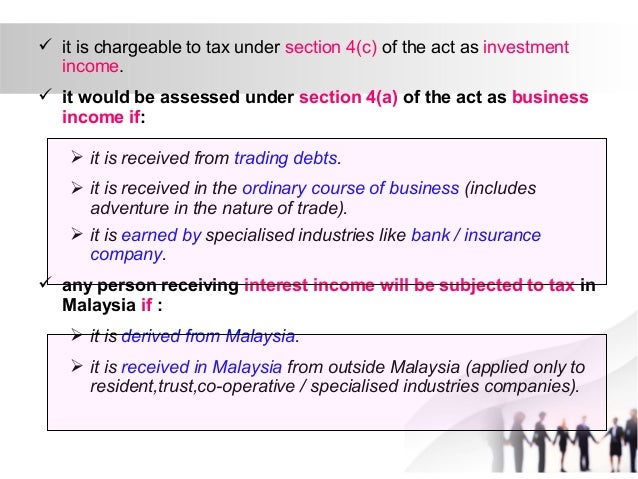

Non chargeability to tax in respect of offshore business activity 3 c.

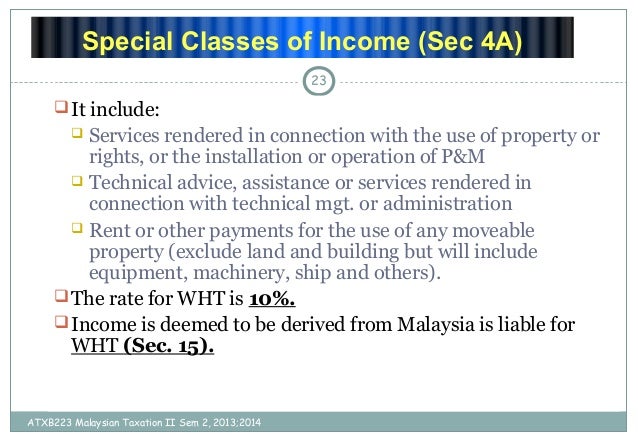

Section 4a income tax act malaysia. I amounts paid in consideration of services rendered in connection with the use of property or rights belonging to. 2 except as provided in subsection 4 a and subsection 4a the estimate of tax payable for a year of. A the responsibility for the payment lies with the government a state government or a local authority. Income under section 4 f refers to gains and profits not covered under sections 4 a to 4 e of the income tax act 1967.

Non chargeability to tax in respect of offshore business activity 3c deleted 4. The special classes of income are those listed in section 4a of the income tax act 1967 ita. Classes of income on. 1 every company trust body or co operative society shall for each year of assessment furnish to the director general an estimate of its tax payable.

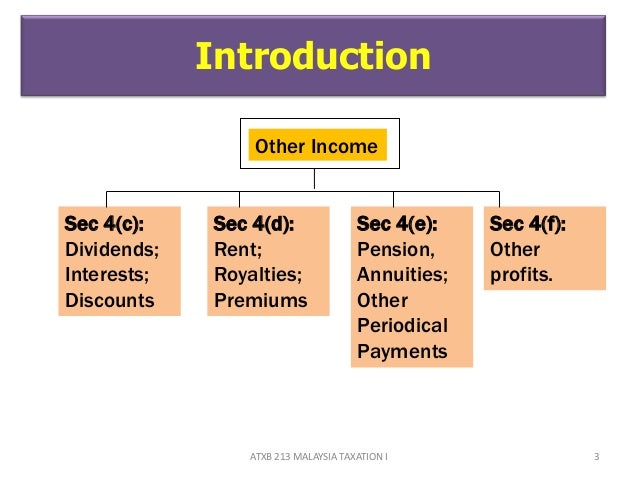

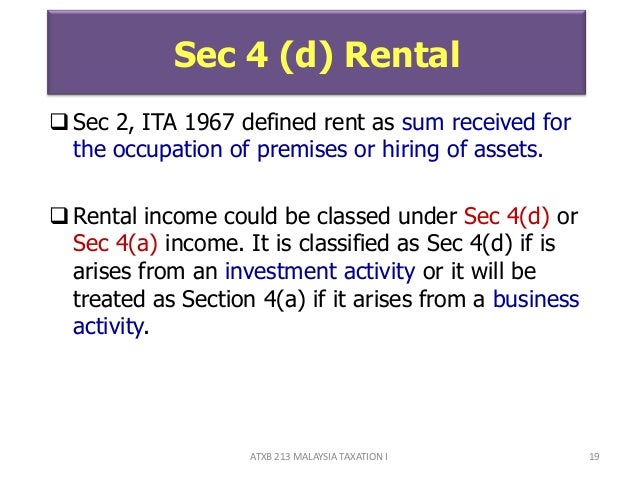

Short title and commencement 2. Charge of income tax 3 a. Section 4 income tax act 1967 in defining income 3 1 introduction 46 3 2 problems 48 3 2 1 each case needs to be decided on its own facts 49 3 2 2 needs extensive proving including calling of witnesses 47 3 2 3 no clear demarcation between revenue and capital 52. Interpretation part ii imposition and general characteristics of the tax 3.

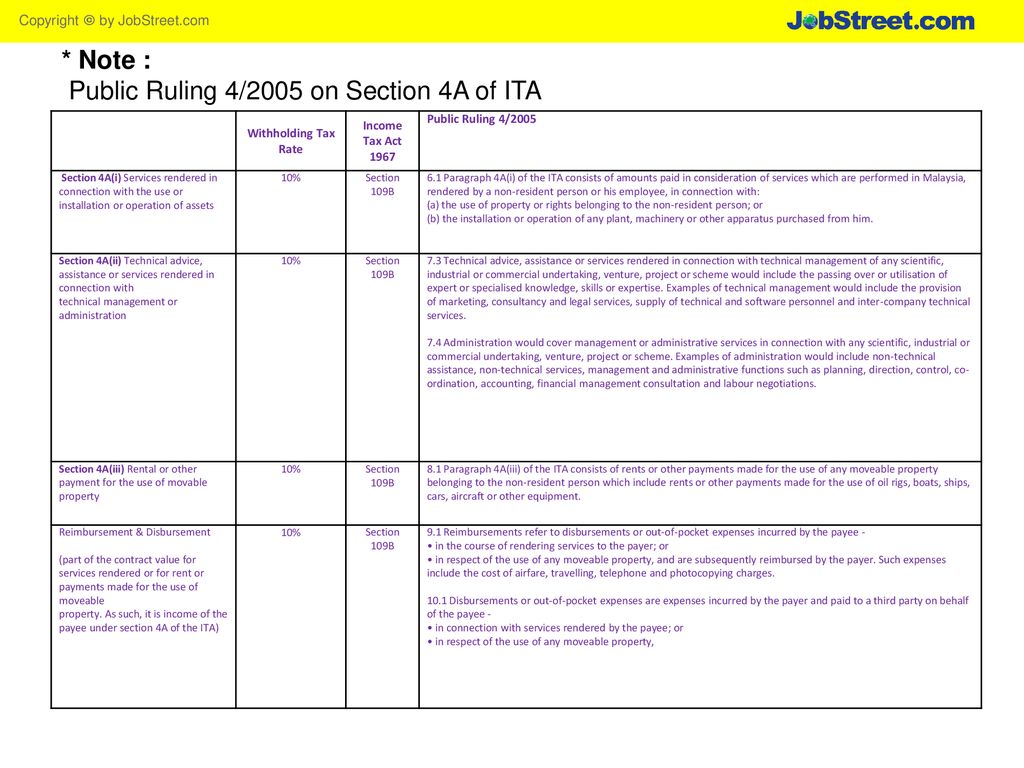

6 1 the gross income in respect of the amounts paid under paragraphs 4a i 4a ii and 4a iii of the ita 1967 shall be deemed to be derived from malaysia if. Section 4a of the income tax act 1967. October 2017 income received by non resident under section 4a i and section 4a ii of the income tax act 1967 ita will not be subject to withholding tax if the services are rendered outside malaysia. With effect from 1 january 2009 a withholding tax mechanism to collect withholding tax at 10 on other types of income of non residents under section 4 f of the income tax act 1967 has been introduced.

Laws of malaysia act 53 arrangement of sections income tax act 1967 part i preliminary section 1. Income that a nonresident derives from malaysia from special classes of income is subject to tax in malaysia. Interpretation part ii imposition and general characteristics of the tax 3. Short title and commencement 2.

5 2 pursuant to section 6 of the finance act 2017 act 785 effective from 17 1 2017 income under paragraphs 4a i and 4a ii of the ita which is derived from malaysia is chargeable to tax in malaysia regardless of whether the services are performed in or outside malaysia. Charge of income tax 3a deleted 3b. Income of a person not resident in malaysia in respect of.

Chapter 6 Business Income Students 1

Chapter 6 Business Income Students 1

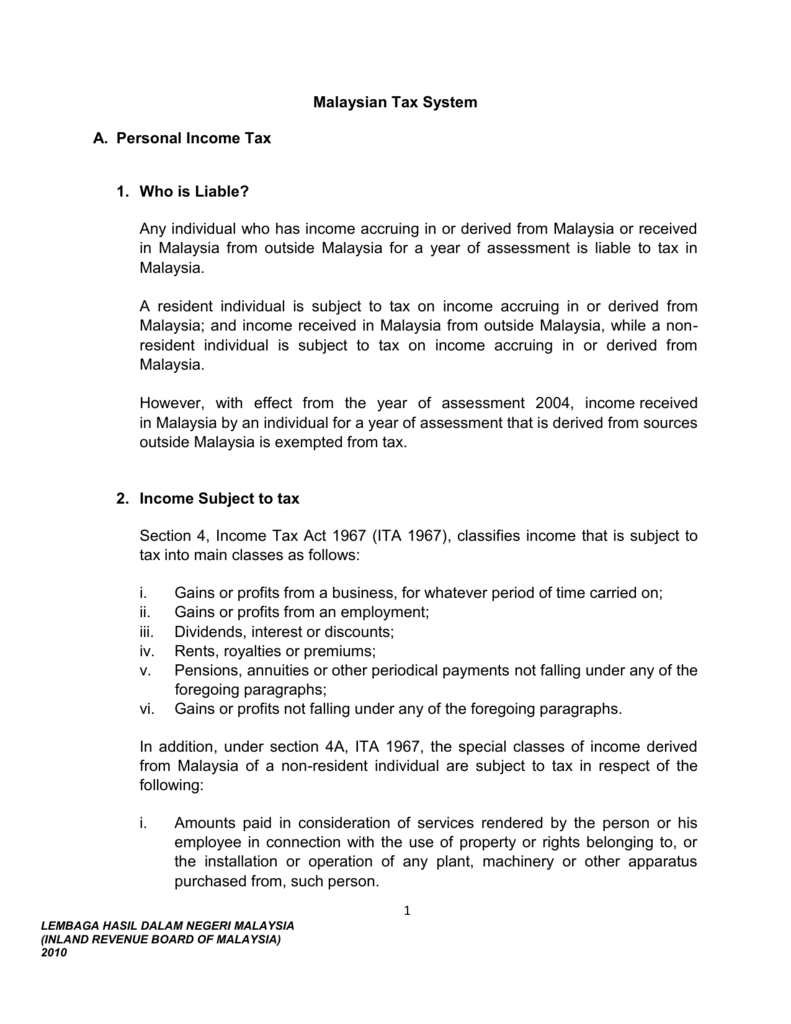

Malaysian Tax System

Problem Based Learning Project Tax Computation On Malaysian Food Service Mfs Sdn Bhd Group B Namematrik No Izwani Bt Abdul Majid Hazwani Bt Ghazali Ppt Download

Taxation Principles Dividend Interest Rental Royalty And Other So

Chapter 5 Non Business Income Students

Problem Based Learning Project Tax Computation On Malaysian Food Service Mfs Sdn Bhd Group B Namematrik No Izwani Bt Abdul Majid Hazwani Bt Ghazali Ppt Download

Tax Planning On Rental Income Afc Chartered Accountants Audit Tax Advisory And Accounting

Introduction To Malaysian Taxation Unit Trust Consultants Ppt Download

Https Assets Kpmg Content Dam Kpmg My Pdf External Tax Finance Bill 2018 Income Tax Amendment 20bill 2018 And Labuan Business Activity Tax Amendment Bill 2018 Highlights Pdf

Problem Based Learning Project Tax Computation On Malaysian Food Service Mfs Sdn Bhd Group B Namematrik No Izwani Bt Abdul Majid Hazwani Bt Ghazali Ppt Download

Problem Based Learning Project Tax Computation On Malaysian Food Service Mfs Sdn Bhd Group B Namematrik No Izwani Bt Abdul Majid Hazwani Bt Ghazali Ppt Download

Which Itr Form You Should File New Income Tax Return Form For Ay 2017 18 Fy 2016 17

Https Www Ey Com Publication Vwluassets Malaysia Issues Practice Note On Tax Treatment Of Digital Advertising Provided By Nonresidents File 2018g 02077 181gbl My 20issues 20practice 20note 20on 20tax 20treatment 20of 20digital 20advertising 20provided 20by 20nonresidents Pdf

Chapter 6 Business Income Students 1

Problem Based Learning Project Tax Computation On Malaysian Food Service Mfs Sdn Bhd Group B Namematrik No Izwani Bt Abdul Majid Hazwani Bt Ghazali Ppt Download

Malaysia Highlights Of The Finance Bill 2016 Conventus Law

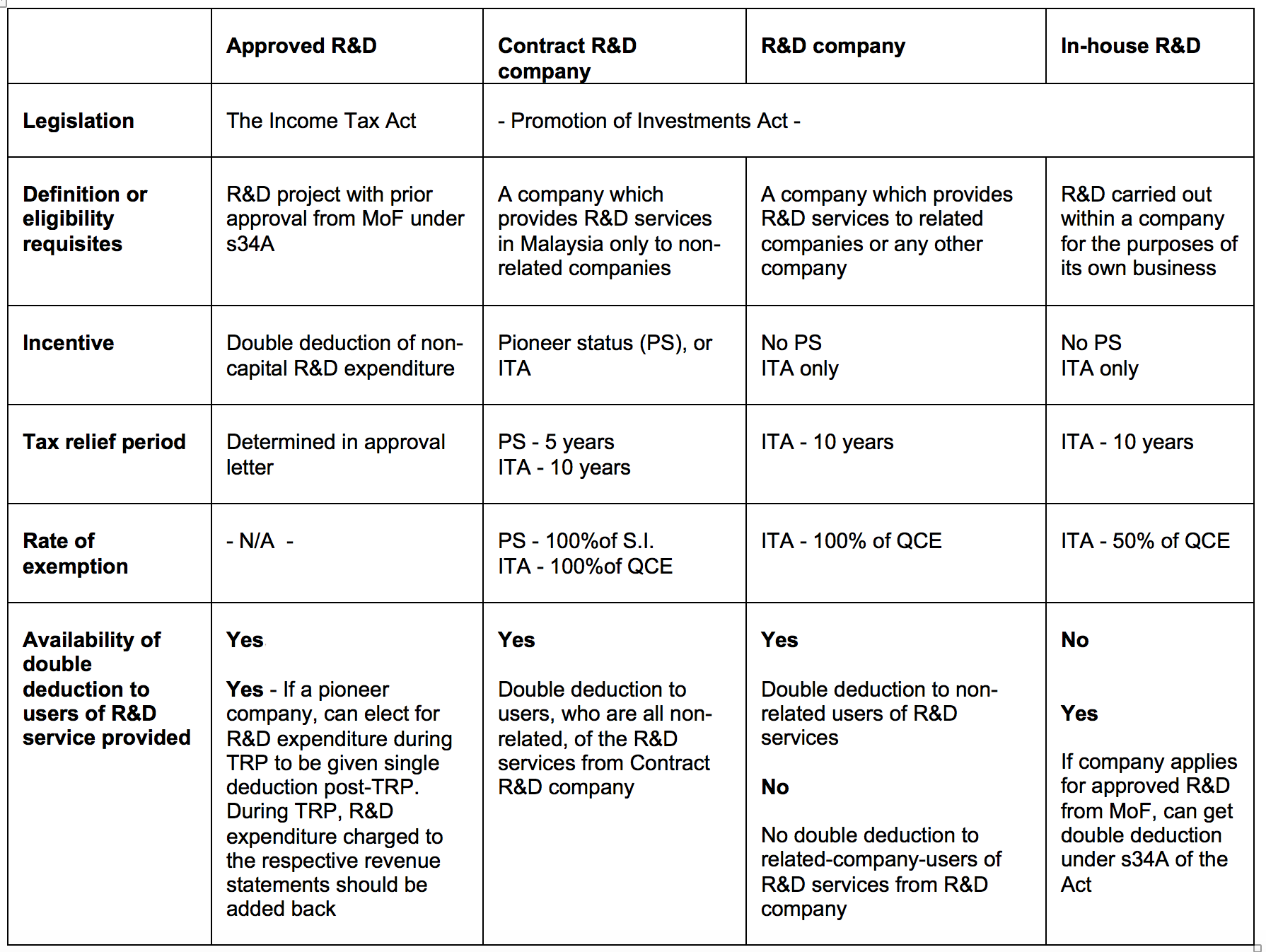

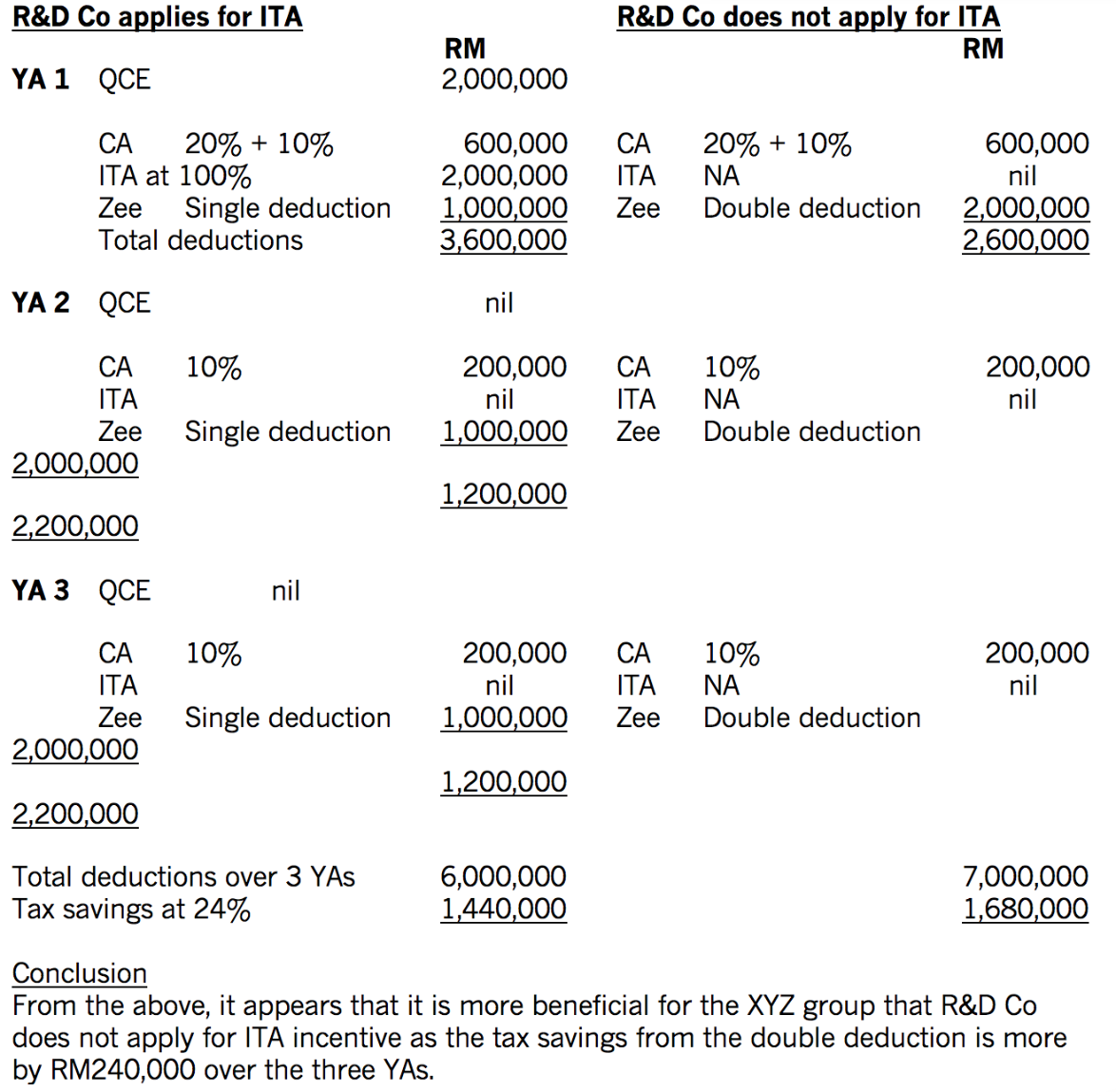

Tax Incentives For Research And Development In Malaysia Acca Global

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcq3x855yub7ypulwiacaylq4xvxau6qcctxmudqhuzbtrqvxq0b Usqp Cau

Pr Po Process Flow By Jace Cheah Ppt Download

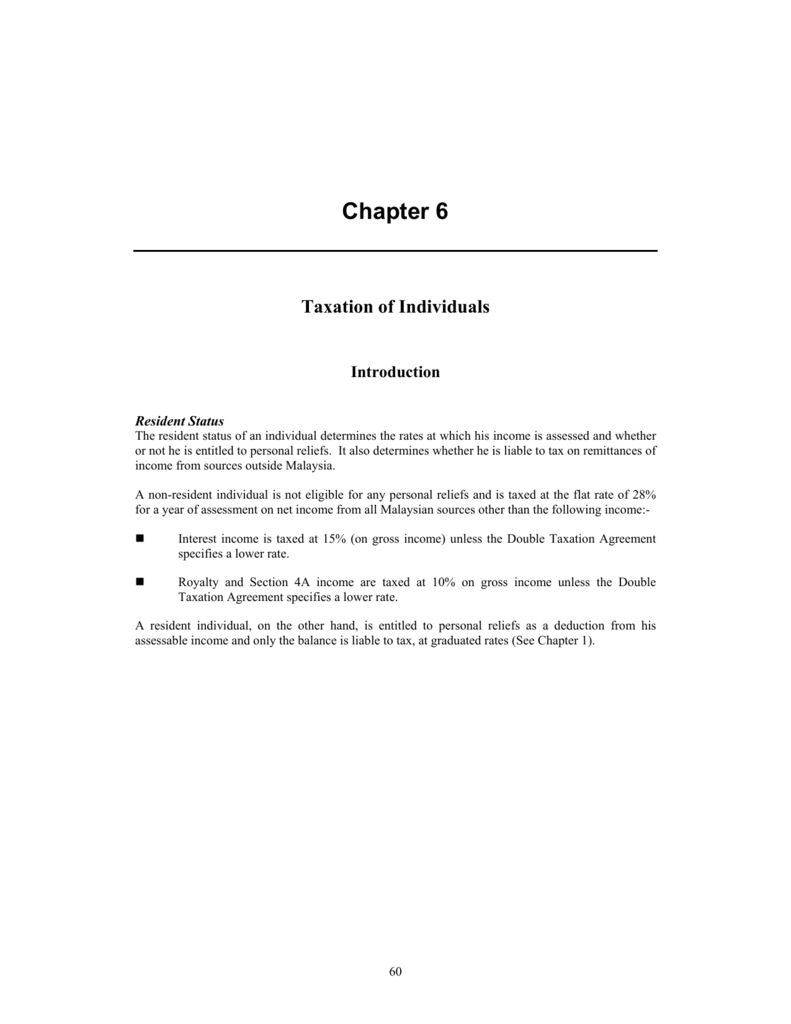

Taxation Of Individuals

Tax Incentives For Research And Development In Malaysia Acca Global

Non Resident Individual Income Tax Lembaga Hasil Dalam Negeri

Withholding Tax On Income Under Paragraph 4 F

Ppt Tutorial 1 Introduction To Income Tax Law Powerpoint Presentation Id 3473088

Https Www Oecd Org Tax Transfer Pricing Transfer Pricing Country Profile Malaysia Pdf

Income Tax Of An Individual Lembaga Hasil Dalam Negeri

Http Www Hasil Gov My Pdf Pdfam Practicenote 01 2017 Pdf

Demystifying Malaysian Withholding Tax Kpmg Malaysia

Cross Border Transactions Chartered Tax Institute Of Malaysia

Http Www Hasil Gov My Pdf Pdfam Samplerf Guidebook C2019 2 Pdf

Chapter 6 Taxation Of Individuals Introduction Pdf Free Download

Schedule 4a Capital Expenditure On Approved Agricultural Projects Pdf Free Download